Mat Credit Entitlement Set Off

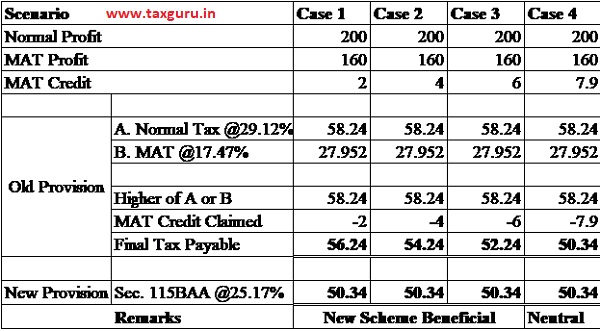

New Corporate Taxation Regime Section 115baa Mat

New Corporate Taxation Regime Section 115baa And Mat

Mat Credit Whether Credit For Surcharge And Education Cess On Brought Forward Mat Credit Is Available The Tax Talk

The Bane Of Mat Credit

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

Prakash Industries Ltd Prakash Stock Opportunities Valuepickr Forum

Suggestion on clause 46 a of finance bill 2017 section 115jaa extension of period of carry forward of mat credit from 10 years to 15 years clarity regarding carry forward and set off of mat credit in cases where the ten year period has expired on or before ay 2016 17 but the fifteen year period has still not expired.

Mat credit entitlement set off.

Standalone Financial Statements Mindtree

Significant Accounting Policies And Notes To The Accounts For The Year Ended March 31 2013 Mindtree

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Consolidated Financial Statements Mindtree

Source : pinterest.com